Introduction to Insurance Archaeology Services, LLC

Property owners, and business owners and operators, may face claims and liability for identified elevated concentrations of contaminants (pollutants) in soil, soil vapor and groundwater resulting from past business operations. Or a business may face liability from asbestos and talc exposures, sexual assault, and other complex business torts. Accordingly, it is imperative that a business or a property owner promptly obtain its previous insurance policies. In the case of environmental (pollution/contamination) exposures, a business or property owners pre-1986 liability and property insurance policies may be able to properly respond to this potential or actual claim. Accessing these older insurance policies can provide policyholders and former policyholders with substantial coverage (i.e., defense and indemnity) against future claims and/or litigation. The past or present policyholder that has full access to its entire insurance portfolio will be better protected and properly prepared to address such contingencies. The specific reason for seeking and collecting pre-1986 liability and/or property insurance policies relative to environmental exposures is that these policies generally do not contain a substantive “pollution exclusion.”

Where environmental (pollution/contamination) issues exist, the goal should often be to try to protect all parties associated or formerly associated with the property. Since a business or property owner can possibly be held jointly and severally liable (responsible) for claims being presented now or in the future, it is very important that our insurance archaeology firm promptly obtain your pre-1986 liability and property insurance information and policies. Under joint and several liability, a claimant may pursue an obligation against any one party as if they were jointly liable and it becomes the responsibility of the defendants to sort out their respective proportions of liability and payment. Joint and several liability is most relevant in tort claims, whereby a claimant may recover all the damages from any of the defendants regardless of their individual share of the liability. This means that if the claimant pursues any one defendant and receives payment, that defendant can then pursue the other obligors for a contribution to their share of the liability. Therefore, a property owner could later become a target defendant. To protect all parties, it is imperative that an insurance archaeology firm obtain the parties pre-1986 liability and property insurance information and copies of the old insurance policies. Thereafter, any such claims presented can be tendered to the parties insurance carrier(s) for appropriate handling (i.e., defense and/or indemnification).

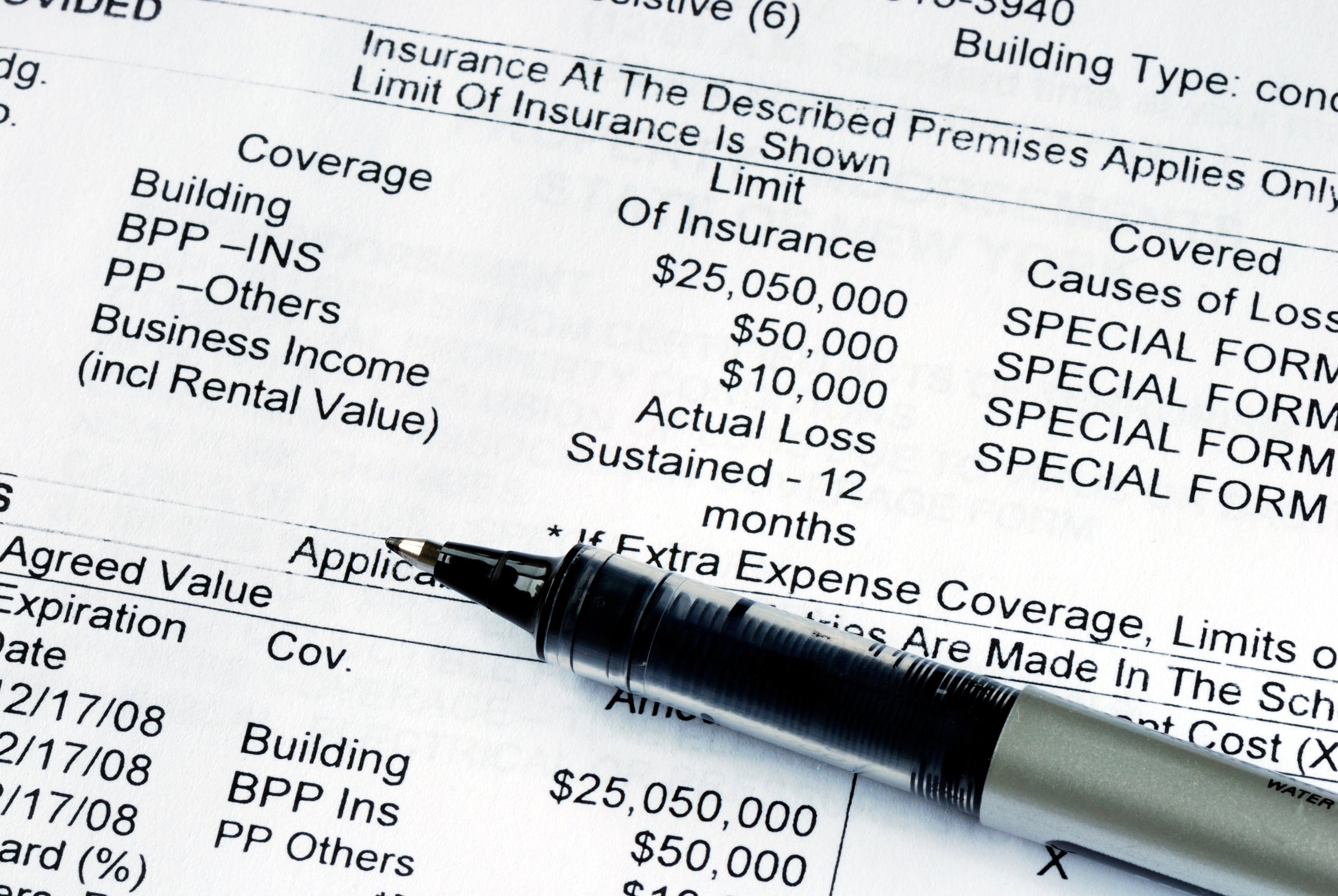

For businesses, the most common type of liability insurance is comprehensive or commercial general liability (CGL) insurance coverage. In the late 1940’s, the “comprehensive” general liability policy was introduced. This policy was intended to insure all risks not specifically excluded. The primary purpose of a comprehensive general liability policy is to provide broad comprehensive insurance. Obviously, the very name of the policy suggests the expectation of maximum coverage. Consequently, the comprehensive general liability insurance policy has been one of the most preferred by businesses and governmental entities over the years because that policy has provided the broadest coverage available. All risks not expressly excluded are covered, including those not contemplated by either party.

Until 1966, standard form CGL policies typically provided coverage for claims alleging two types of damage or injury - “bodily injury” and “property damage.” After 1966, it became common to find CGL policies that also provided coverage for “personal injury” and “advertising injury.” Indeed, since at least the early 1980’s, standard form CGL policies have included coverage for all four (4) types of injury.

A typical CGL policy obligates the insurance company to pay those sums that the policyholder becomes legally obligated to pay as damages because of bodily injury or property damage to which the policy applies. The insurance applies only to bodily injury and property damage which occurs during the policy period. The “bodily injury” or “property damage” must be caused by an “occurrence.” The “occurrence” must take place in the “coverage territory.”

It also typically obligates the insurance company to defend any “suit” seeking those damages. This may include defending its policyholder (and others) against any future claim that is presented. CGL policies are, by far, the most important form of insurance coverage available to most policyholders.

Liability insurance policies provide insurance for specifically described persons and entities. Typically, there is a “named insured,” which will be the corporate entity. In a provision entitled “Who is an Insured” the policy may describe other persons (such as employees or shareholders) or entities (such as vendors) who will be considered “insureds” under the policy. Liability policies also may extend coverage to other parties, generally listed in an endorsement. Often these “additional insureds” will include corporate affiliates of the “named insured,” or persons or entities with whom the named insured has a close commercial relationship, or to whom the named insured is contractually bound to provide insurance.

The policy and the law require that, for the insurer’s duty to defend [you] to trigger, the insurer must be placed “on notice” of a claim. Typically, standard notice language provides that notice be given to “the company or any of its authorized agents. The standard notice language in a policy also requires that notice of an occurrence be given “as soon as practicable” and that, in the event of a claim or lawsuit, you immediately forward “every demand, notice, summons or other process” received. Therefore, it is very important to timely identify these insurance companies and to quickly provide them with notice of any actual or future claim.

Standard notice language in a CGL policy usually requires, at least, the following information:

1. Your identity;

2. Information relating to the time, place and circumstances of the occurrence; and

3. The names, addresses of the insured and of available witnesses.